However, there are some additional adjustments that can be made to help defer income to future years. It is important to note that the confusion coming with this accounting practice can lead people to deception of financial statements. For example, some businesses have misused the method to hide weaknesses and mistakes within their financial reports.

Accruals – What Are Accruals?

Your business might not need someone with vast experience in accounting to be in charge of your books, but cash basis won’t give you complete insight on how your business is actually performing. To compute the sales test, a company averages revenue from the last three years. If the average is less than the $1 million threshold, the cash method is always allowed (but not required).

Can be more complicated to implement since it’s necessary to account for items like unearned revenue and prepaid expenses. Including accounts receivables and payables allows for a more accurate picture of the long-term profitability of a company. Here are the advantages and disadvantages of both accounting methods. The key difference between the two methods is the timing in which the transaction is recorded.

We’ll cover the benefits and disadvantages of the two methods, and by the end of this article, you should have a clearer picture of whether cash or accrual accounting best suits your needs. With Debitoor, expenses and revenues are categorised and organised quickly and easily. The system automatically matches transactions with bank statements and balances cash inflow and outflow.

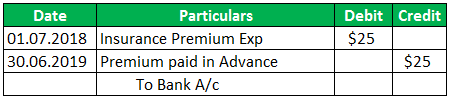

Now consider the following three cases in which John pays cash to Sam and records rent expense. This example displays normal balance how the appearance of income stream and cash flow can be affected by the accounting process that is used.

Under the old procedure, the time for filing was the first 180 days of the tax year. The IRC section 481-a adjustment period in general, is four years, beginning with the year of change for both positive and negative adjustments. At the same time, the accounting data is ‘bias-free’ since the accounting data are not subject to the bias of either management retained earnings balance sheet or of the accountant who prepares the accounts. In other words, the Objectivity Principle requires that each recorded transaction/event in the books of accounts should have adequate evidence to support it. This concept calls for an adjustment to be made in respect of prepaid expenses, outstanding expenses, accrued revenue, and unaccrued revenues.

Accrual basis accounting allows you to share more meaningful information with business partners and associates. Keep in mind that depreciation is a noncash expense because the cash outlay already occurred accrual accounting when the asset was purchased and recorded on the balance sheet. If you’re the head of your company and you’re handling bookkeeping too, keeping up with accounting accrual might prove to be too much work.

Cash Basis Accounting Vs. Accrual Accounting

During the month, the company pays its employees, it fuels its generators, and it incurs logistical costs and other overheads. Accrued revenues are either income or assets (including non-cash assets) that are yet to be received. In this case, a company may provide services or deliver goods, but does so on credit.

Can you switch from accrual to cash accounting?

Two concepts, or principles, that the accrual basis of accounting uses are the revenue recognition principle and the matching principle.

Patriot’s online accounting software is easy-to-use and made for the non-accountant. Accrued liabilities are usually recorded at the end of an accounting period. Accounts payable is recorded based on invoices during the normal course of business. If by now, you’re thinking accrued expenses sound a whole lot like accounts payable, you’re right. Accrued expenses and accounts payable are similar, but not quite the same.

- Unless a statement of cash flow is included in the company’s financial statements, this approach does not reveal the company’s ability to generate cash.

- If a business records its transactions under the cash basis of accounting, then it does not use accruals.

- Under accrual accounting, financial results of a business are more likely to match revenues and expenses in the same reporting period, so that the true profitability of a business can be recognized.

The new automatic change procedure—revenue procedure 97-37—generally provides for a four-year adjustment period consistent with revenue procedure 97-27. Some exceptions result in a shorter or accelerated uniform four-year adjustment period. The section 481(a) adjustment is not prorated for the shorter period. If the entire adjustment is less than $25,000 (either positive or negative), the taxpayer may elect a one-year adjustment period.

Cash Basis Accounting

In historical cost accounting, the accounting data are verifiable since the transactions are recorded on the basis of source documents such as vouchers, receipts, cash memos, invoices, etc. It is wrong to recognize revenue on all sales, but charge expenses only on such sales as are collected in cash till that period. Like revenue accounts, expense accounts are temporary accounts that collect data for one accounting period and are reset to zero at the beginning of the next accounting period.

What It Means To “Record Transactions”

A cash flow statement is a financial statement that provides aggregate data regarding all cash inflows and outflows a company receives. Accrued revenue—an asset on the balance sheet—is revenue that has been earned, but for which no cash has been received. Accruals improve the quality what are retained earnings of information on financial statements by adding useful information about short-term credit extended to customers and upcoming liabilities owed to lenders. If you’re considering changing your accounting method, contact Matt or your trusted BKD advisor for more information.

What are the key principles of accrual accounting?

Accruals are needed for any revenue earned or expense incurred, for which cash has not yet been exchanged. Accruals improve the quality of information on financial statements by adding useful information about short-term credit extended to customers and upcoming liabilities owed to lenders.

Let’s begin our analysis of your beginning balance sheet with the liabilities and owner’s-equity sections. We’re assuming that, thanks to a strong business plan, you’ve convinced a local bank to loan you a total of $125,000—a short-term loan of $25,000 and a long-term loan of $100,000. Naturally, the bank charges https://myreca.app/2019/07/10/ripoff-report-1800accountant-llc-review/ you interest (which is the cost of borrowing money); your rate is 8 percent per year. In addition, you personally contributed $150,000 to the business (thanks to a trust fund that paid off when you turned 21). An expense is recognized on the income statement when it’s incurred, regardless of when payment is made.

This matches the expense of the products to the same period as the revenue the products generated. The timing of when you paid for the products does not affect when you record the expense. Percentage completion uses the costs incurred to date divided by the total estimated contract costs. The percentage is multiplied against the estimated contract revenue to arrive at the revenue earned for that year.

A sale is recognized on the income statement when it takes place, regardless of when cash is collected. Record of cash owed to sellers from whom a business has purchased products on credit. Garcia received her Master of Science in accountancy from San Diego State University.

The Effect On Taxes

Let’s look at an example of a revenue accrual for an electric utility company. The utility company generated electricity that customers received in December. However, the utility company does not bill the electric customers until the following month when the meters have been read. To have the proper revenue figure for the year on the utility’s financial statements, the company needs to complete an adjusting journal entry to report the revenue that was earned in December. Accruals and deferrals are the basis of the accrual method of accounting.

Advertise Here